There is a lot of jargon that is thrown around in the world of finance and business valuation. This blog post attempts to lift the veil on some of the more commonly used finance & business valuation terms. Although there are many, many more terms that could be included on this list, these listed below are but a sample....

1. EBITDA – it stands for Earnings Before Interest, Taxes, Depreciation and Amortization. To calculate the EBITDA of a business you would take the net income of the business and add back the interest expense, income taxes, depreciation & amortization. EBITDA is an “unlevered” measure of profit – it is a profit measure before interest expense is deducted. It is intended to be a proxy for pre-tax cash flow but it does have some deficiencies such as not accounting for capital expenditures, changes in net working capital or differing tax rates.

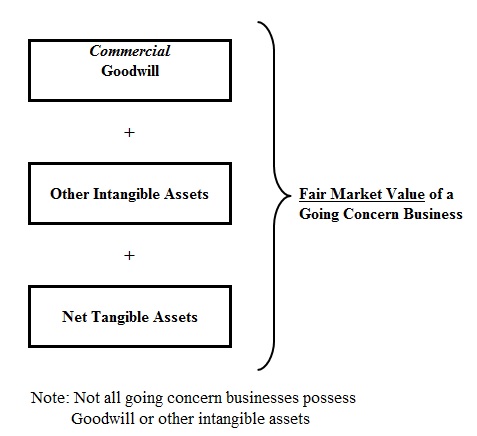

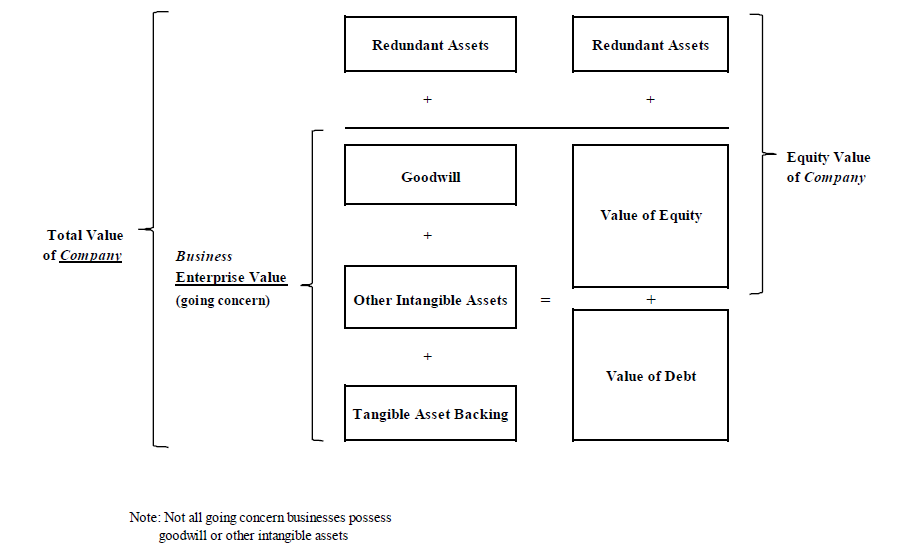

2. Enterprise Value – in business valuation, Enterprise Value (EV) refers to the total value of a company, its debt and its equity combined. The theory is that EV is a measure of a company's total worth without the 'noise' associated with its capital structure. Using a house as an analogy... if your home was appraised to be worth $1 million and you had a $600,000 mortgage on it then the 'EV' of your house would be $1 million and the equity value of the home would be $400,000 ($1 million less $600,000). To calculate the equity value of a business you would subtract business debt from its EV.

A commonly used business valuation ratio is the Enterprise Value / EBITDA ratio. Example - if a business is valued at $400,000 Enterprise Value and has an EBITDA of $100,000 then the EV/EBITDA ratio would be 4x. This ratio could then be compared to industry peers.